Can the Kiwi Hold On as RBNZ Pauses and Tariffs Bite?

New Zealand’s economy is showing clear signs of deceleration, and the Reserve Bank of New Zealand (RBNZ) is taking a breather after an aggressive round of rate cuts. The country slipped into a deeper-than-expected recession late last year, with GDP contracting 1% in the three months through September 2024. Since then, the economy has been on a slow road to recovery, one that is fragile but gradually stabilising.

However, global headwinds remain, with Trump’s tariff spree continuing to rattle policymakers. The latest round of U.S. tariffs, targeting strategic items like copper, triggered a surge in copper futures amid concerns over supply disruptions. For New Zealand, which relies heavily on trade, these tariffs could weigh on economic growth and dampen external demand.

Domestically, challenges persist in the labour market. Employment growth is sluggish, coming in at just 0.1% in Q1, while unemployment held steady at 5.1%. Wages are softening, and consumer sentiment remains fragile.

For the RBNZ, this means that while they are near the end of their rate cutting cycle, they might not be just done yet. While the central bank held its official cash rate steady at 3.25% yesterday as widely expected, markets are pricing in one or two more 25bps cuts by year-end, largely to offset the impact of weakening global demand and trade tensions.

For traders, this means short-term pressure may persist on the Kiwi dollar (NZD), given the lower interest rate outlook. However, if risk appetite returns and global trade stabilises, we could see renewed interest in the NZD, especially as a pro-cyclical, commodity-linked currency.

Going forward, watch out for any indications of further monetary easing from the RBNZ. At the same time, understanding global risk sentiment will be important for commodity currencies such as the NZD, which tends to perform better in periods of risk-on sentiment.

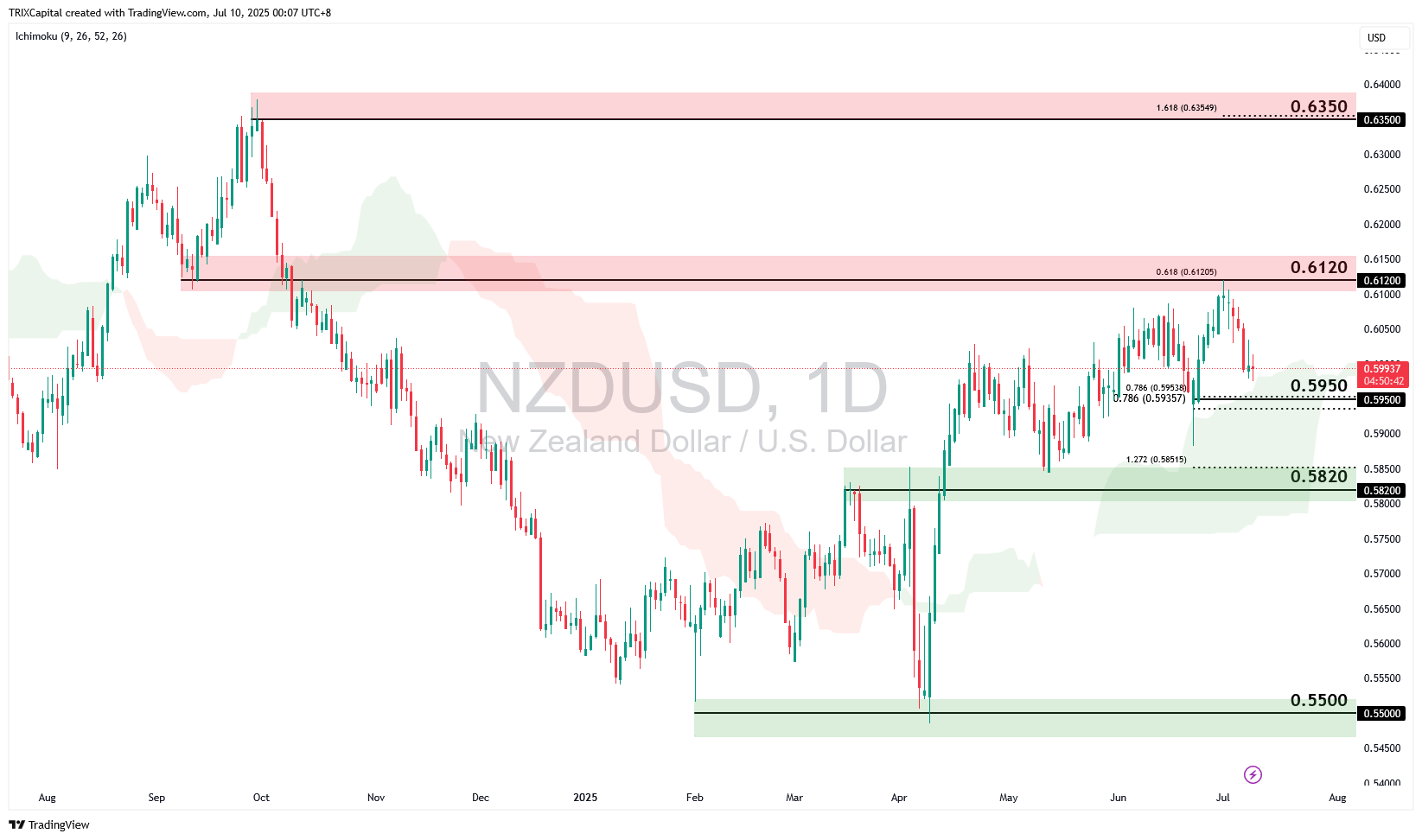

NZDUSD Stalls Below Key Resistance

NZDUSD is now testing a key resistance zone at 0.6120, aligning with the 61.8% Fibonacci Extension. The pair is trading above the Ichimoku cloud, suggesting bullish momentum remains intact. A break and close above 0.6120 could pave the way for further upside toward 0.6350, near the 161.8% Fibonacci Extension and previous swing high.

However, a deeper retracement could see the price revisit the support zone at 0.5950, which aligns with a key area of Fibonacci confluence and the Ichimoku cloud. A more extended pullback could bring the price down toward the 0.5820 support level, in line with the 127.2% Fibonacci Extension.

NZDJPY Drifts Sideways Amid Waning Kiwi Strength

NZDJPY has been trading in a sideways range since June, consolidating between key resistance and support levels. Despite the sluggish momentum, the price remains supported above the Ichimoku cloud, suggesting that the bullish structure is still intact for now.

Should momentum pick up, a move toward 89.30 could be on the cards. This level aligns with both the 78.6% Fibonacci retracement and 61.8% Fibonacci extension, making it a key resistance level to watch. A confirmed break and close above this zone could open the path to 92.30, the 100% Fibonacci extension and the next major upside target.

However, downside risks are growing. A firmer Japanese yen, underpinned by hawkish expectations for the Bank of Japan, especially following an unexpected surge in Japan’s household spending data, could weigh on NZDJPY. In such a scenario, the price may drift back toward support at 86.40 and potentially 84.50, both of which sit near areas of strong Fibonacci confluence. With the RBNZ nearing the end of its easing cycle and global trade tensions still weighing on sentiment, the outlook for the Kiwi remains delicately balanced. While soft domestic data and ongoing tariff pressures suggest downside risks, any signs of stabilisation in global demand or a shift in risk sentiment could quickly breathe new life into NZD pairs. In the near term, stay focused on RBNZ signals, global commodity flows, and shifts in risk appetite.